In today's interconnected world, where families and communities are scattered across different countries, remittance has emerged as a lifeline, fostering connections, and fueling economic growth. Remittance is money transferred by migrant workers to their people living in their home countries, which plays a pivotal role in supporting the well-being of millions of individuals and shaping the economies of both sending and receiving nations. As we delve into the fascinating realm of remittance, we uncover a powerful force that not only bridges physical distances but also empowers families, stimulates investment, and drives development. Join us as we explore the profound impact of remittance on people's lives and the larger socio-economic landscape in this enlightening blog.

What is Remittance Transfer?

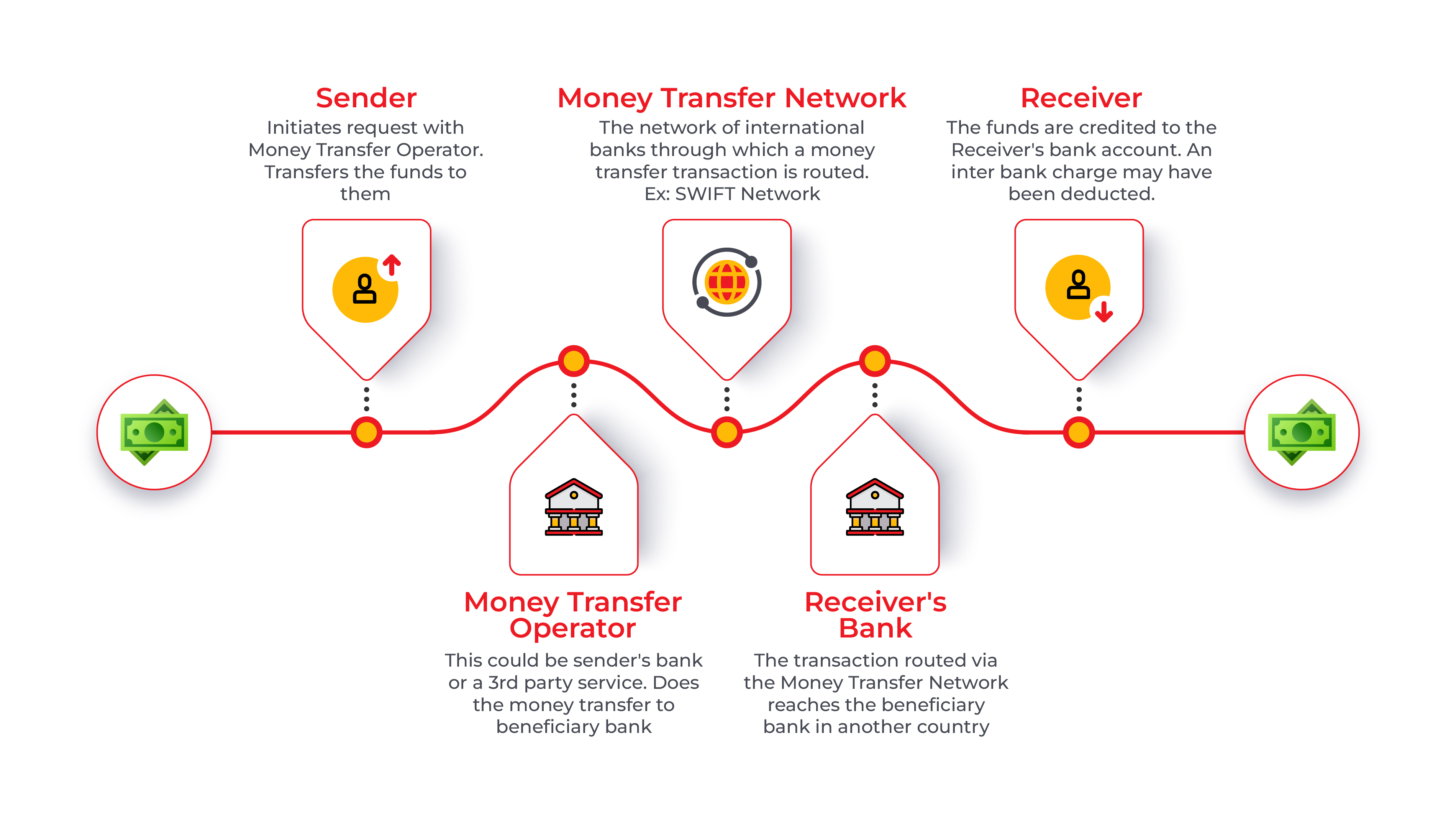

The term is derived from the word “remit” which means to send back. Thus, the transfer of funds from the sender to the receiver is called remittance. Remittances are generally considered as the overseas transfer of funds. Online Remittance can be used for various purposes, such as paying invoices for business or funds transfers to family or friends. The most common way of sending remittances is through an electronic payment system of money transfer services. Remittance serves as a basic livelihood serving the needs of families in developing countries. These services can be accessed through service institutions, fund transfer operators or online payment platforms, making it convenient for sending money and receiving money. There are four Parties that are actively involved in online remittances.

- Sender/Remitter

- Receiver/Beneficiary/Recipient

- Sending Agent

- Receiving Agent

Common Types of Remittance

Now that we have learned about the meaning of Remittance and its effect on the socioeconomic development of a nation. Let’s dig deeper into the types of Remittances. Generally, there are two types of online remittance:

Outward Remittance

When a Remitter transfers funds out of the country, then it is known as an outward remittance. For instance, if a family member transfers money to their children living abroad, then this outward flow of funds with called outward Remittance. Outward Remittance is applicable to the countries from where the funds are being sent.

Inwards Remittance

Inward Remittance is the transfer of funds from within the country or from across borders. If a family has children working in different countries, and they send money to their home, then it is known as inward Remittance.

How can Remittance be Collected?

It's important for both sender and recipients to choose a remittance service offering a convenient, secure, collection method that aligns the preferences of both parties. The availability of collection methods may vary depending on the remittance service providers, local regulations, and the level of financial infrastructure in the receiving country. Here are some common ways in which remittances can be collected.

Cash Pickup: Cash pickup is a popular method, particularly in regions with limited access to formal financial services. The recipient can visit a designated cash pickup location, to collect the remittance in cash. It is a secure process that requires identification documents and a transaction reference number.

Bank Deposits: Remittances can be directly deposited into the recipient's bank account. The sender needs to provide the necessary information, such as the recipient's account number and other bank details, to initiate the transfer. The recipient can then access the funds by visiting the bank or using their debit card to withdraw money.

Mobile Money Services: Mobile money services have gained popularity as a convenient and accessible way to collect remittances, particularly in areas with limited banking infrastructure. To successfully receive the fund, the recipient needs to have a mobile money account, with a mobile network operator, or any third-party app that provides the feature of online Remittance. The remittance is transferred directly into the recipient's mobile money account, and they can access the funds using their mobile phone.

Prepaid Debit Cards: Some remittance providers offer prepaid debit cards that can be loaded with the remittance amount. These cards work similarly to regular debit cards and can be used at ATMs, point-of-sale terminals, or online platforms to withdraw cash, make purchases, or transfer funds to other accounts.

Digital Wallets and Online Platforms: With the growth of digital financial services, remittances can be collected through digital wallets or online platforms. The recipient can have a digital wallet account or use online payment platforms to receive and manage the remittance funds. These platforms may offer options for transferring funds to a bank account, making online purchases, or even converting the funds into local currency.

Advantages of Remittance

Over the period, Remittance has become an imperative component of the global financial system. Here are a few most common benefits of sending/receiving Remittances.

- Family Support: For certain families, remittance is the primary source of survival. With the earning member living outside the country, families wait for money from them to meet their basic needs such as food, education, healthcare etc. When households receive remittances, it helps alleviate poverty by providing a source of income. The families at the receiving end, move out of poverty and their purchasing power increases, enabling them to engage in more economic activities. This uplifts local economies and contributes to overall economic growth.

- Economic Stimulation: International Remittances have a notable impact on economic stimulation for both the sending and receiving countries. Remittances inject additional funds into the receiving country's economy, increasing consumption and creating a ripple effect of economic activity. Remittances can be used for investment purposes, such as starting or expanding businesses, funding startups investing in property, or funding entrepreneurial ventures. These investments generate employment, promote entrepreneurship, and foster economic development.

- Convenience and Accessibility: Remittance services have made significant advancements in terms of convenience and accessibility, benefiting both senders and recipients. Today, senders and recipients have access to a wide range of transfer channels, including online platforms, mobile apps, and digital wallets. These options offer convenience by allowing transactions to be initiated and completed remotely, anytime and anywhere with internet access. Mobile money services enable users to send, receive, and store money through their mobile devices.

- Poverty Reduction: Remittances often contribute to investments in human capital, such as education and healthcare. Families can use the funds to pay for school fees, purchase books, uniforms, or cover medical expenses. By investing in education and health, remittances can break the cycle of poverty by empowering individuals to secure better job opportunities and improve their overall well-being. Many recipients of remittances use the funds to invest in entrepreneurial ventures, which can create employment opportunities, generate income, and contribute to local economic development. These businesses often have a positive impact on poverty reduction by lifting families out of poverty.

- Long Term Growth Potential: Remittances can have long-term growth potential for both the sending and receiving countries. Here are some ways in which remittances can contribute to long-term economic growth: Investment and Entrepreneurship, Human Capital Development, Savings and Investments, Financial Sector Development, enhancement of Technology and Innovation and Diaspora Engagement etc. Remittances can support social and community development initiatives that contribute to long-term growth.

How Does Remittance Work?

Step 1 Sender or Remitter Initiates the Remittance, they connect with the remittance service provider, such as a bank, money transfer operator, or online remittance platform, to send money to the recipient. The sender provides the necessary information including the recipient's information and the preferred collection method for the remittance.

Step 2. If the currency differs from the recipient's local currency, the remittance service provider converts the funds into the local currency based on the prevailing exchange rate.

Step 3. The converted funds are then transferred to the recipient's country through various banking or payment networks, often involving correspondent banks and intermediaries.

Step 4. Once the funds are transferred, the remittance service provider notifies the recipient about the availability of the remittance through SMS, email, or other communication channels.

Step 5. The recipient follows the instructions and collects the remittance through the collection method chosen by the sender. Throughout the remittance process, remittance service providers ensure compliance with regulations, adhere to anti-money laundering (AML) and know-your-customer (KYC) requirements, and prioritize the security and confidentiality of the transactions.

How can Pay10 help in Online Remittance?

Pay10 is the leading payment gateway rendering multifaceted online payment solutions with an innovative and ultra-proficient approach. We are passionate about making digital payments easy, accessible, and secure with cutting-edge technology aiming to revolutionise the Fintech industry. Our services include a secure payment gateway, e-payment wallets, e-commerce services, online remittance, and merchant accounts. We are among the reputed digital payment service providers that foster secure payment transactions with top-of-the-line industry standards offering unparalleled security. Start your payment journey with us now.